Sales grew 3.9% on a trailing 12-month (TTM) basis. That is as good as analysts had expected. What is impressive is that sales growth is accelerating: a year ago, growth was 120 bp lower (2.7%; data in the next three charts is from FactSet).

Earnings grew more quickly than sales, at 9.2% (TTM). That also represents an accelerating trend: a year ago, earnings were growing 300 bp slower (6.2%).

The faster growth in earnings reflects widening margins, to 9.9% (TTM). A year ago, margins were 40 bp lower (9.5%).

Detractors will immediately claim that these figures reflect excessive corporate buybacks. But over the last two quarters, the effect of buybacks has significantly waned: EPS adjusted for share count would be just 1.5% lower. It's negligible, at least in part because buybacks are mopping up the increase in shares due to stock options given to executives.

The expansion in margins is perhaps the biggest surprise of 2014. Many (including us) did not think margins would continue to grow. Margins were already historically high by the end of 2013; surely they would "mean revert" as they always have in the past. They did not.

With the dollar higher and oil lower, expectations for 4Q have been severely lowered. Analysts expect sales to grow just 1.5% and earnings to grow just 3.4% year-over-year (yoy); at the start of the quarter, those growth rates were expected to be 3.7% and 8.5%, respectively. The tapering in growth in 4Q is seen in the first two charts above.

The S&P is up close to 12% in 2014. Where has this performance come from? You can answer that two ways: one based on sales and the other based on EPS. Let's look at each below.

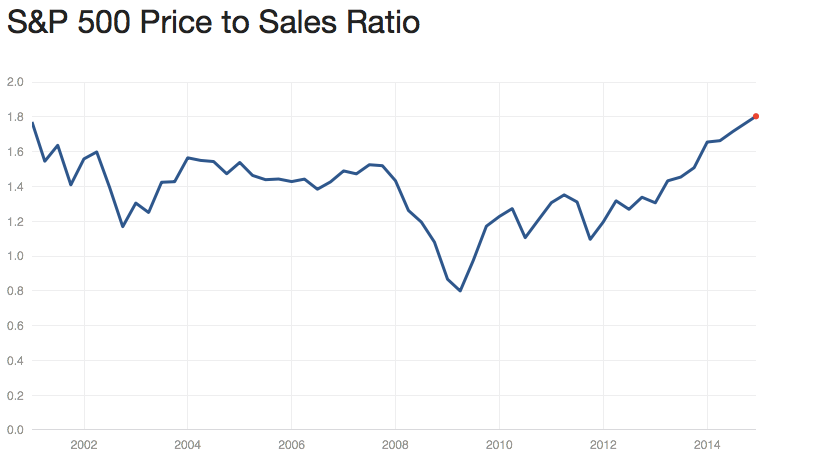

Sales-basis: Sales growth accounts for just 35% of the appreciation in the S&P this year; the remaining 65% is the expansion in price/sales multiples.

At the end of 2013, the index was trading at a price/sales of 1.63x; that has now grown to 1.75x. These price/sales multiples are quite high: 1.6x was the peak of the prior bull market and current valuations are like those from the height of the tech bubble (chart data below from Standard & Poor's).

Earnings-basis: Earnings have been so strong that they account for about 70% of the appreciation in the S&P this year; the remaining 30% is the expansion in price/earnings multiples.

At the end of 2013, the index was trading at a P/E (TTM) of 16.9x; that has now grown to 17.4x. Like price/sales, these P/Es are quite high; 16.5x was the peak of the prior bull market and the long run average is closer to 15.5x. (chart below from FactSet). Historically, a decline in EPS caused P/Es to move higher than they are today (for an explanation of this, read here).

The bottomline is that companies in the S&P are doing very well, much better than expected. The acceleration in sales and expansion in margins is very encouraging.

Is this as good as it gets? Maybe, but that was a widely shared view last year as well. Until margins actually show a decline and sales show a deceleration in growth, it's too early to say the best is in the past. The most obvious head wind heading into 2015 is valuation multiples, but these too are continuing to expand as growth, on the top and bottom line, accelerates.

If you find this post to be valuable, consider visiting a few of our sponsors who have offers that might be relevant to you.