Overall, fund managers remain very bullish on risk. In September, exposure to global equities was the second highest since the survey began in 2001; it is only marginally lower now and it has increased every month since October. What is particularly remarkable is how long managers have been highly overweight equities (virtually all of 2013). This is longer than any period during the 2003-07 bull market.

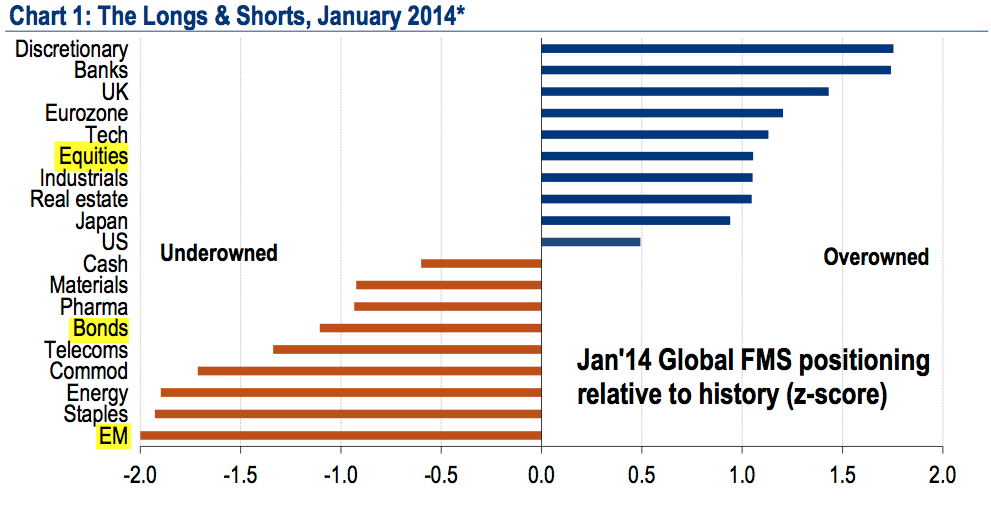

Fund managers are not just overweight equity and underweight bonds, they are overweight the highest beta equity (tech, banks, discretionary) and underweight defensives (telecom, staples, pharma) as well as cash.

Their current exposure to technology (+42%) is the highest of all sectors, while their exposure to staples (-32%) is the lowest since 2003. If there is a silver lining, exposure to tech has stayed high as long as 6 months (and as short as one month) in a row in the past.

Their exposure to banks (+16%) is 1.7 standard deviations above the 10 year average and the 2nd highest since 2006.

In the past, when managers have been this overweight growth sectors like industrials, those sectors have underperformed until their exposure has been reduced. Conversely, when their exposure to safer, income producing sectors like consumer staples has been this low, those sectors have outperformed. So, while current (bullish) market psychology is biased towards high beta, lower beta is likely to outperform in the months ahead.

Managers have their largest overweight position in Eurozone equities, up more than 170% since August. Exposure to Japanese equities is among the highest since 2006.

Emerging markets have been underperforming SPX for a year. There was a two month rally over the summer that began when exposure was the lowest since the survey began in 2001. That rally faded after managers became 1% overweight. Funds are now back to exposure 2.0 standard deviations below the 10 year average. Says BAML: " EM capitulation is close. Rarely have bullish growth expectations mixed with such bleak EM weightings."

You can see from the data that it should mostly be looked at from a contrarian perspective. Fund managers were overweight EEM more than any other market at the start of 2013, and it was the worst performer of the year. In comparison, they were 20% underweight Japan in December 2012 and it was the best equity market in 2013. Now, the big overweight is in Europe.

Survey details are below.

- Cash (+4.5%): Cash balances remained 4.5% (it has been between 4.4% and 4.6% since July 2013). For comparison, it was 3.8% in January and February 2013 when the rally was getting started. Typical range is 3.5-5%. BAML has a 4.5% contrarian buy level but we consider over 5% to be a better signal. More on this indicator here.

- Equities (+55%): A net 55% are overweight global equities (+1.1 standard deviation above 10 year average). It had been up every month since May, but, after reaching the second highest equity weighting ever in September, it unsurprisingly declined in October to 49%. It has now increased three months in a row. In comparison, it was 35% in December 2012 when the rally was still young. More on this indicator here.

- Bonds (-62%): A net 62% are now underweight bonds (-1.1 standard deviation below 10 year average), a slight improvement from November and December. It was -69% in November, tied with April 2006 for the lowest reading ever. For comparison, they were 38% underweight in May.

- Regions:

- Europe (+41%): Europe is the most preferred region for the 5th month in a row. Managers are 41% overweight, a huge increase from 3% overweight in July and 8% underweight in May and April 2013. It was 46% overweight in October, the highest weighting since June 2007.

- Japan (+26%): Managers are 26% overweight Japan. It was 34% in December, the highest weighting since May 2006. Funds were 20% underweight in December 2012 when the Japanese rally began.

- US (+6%): Managers were neutral on the US in October, a big drop from 30% overweight in August, but this increased to 7% overweight in November and December. August was the third highest US weighting ever.

- EEM (-15%): Managers are back to 15% underweight EEM (-2.0 standard deviation below 10 year average). It had increased two months in a row (10% underweight in October, 1% overweight in November) before falling back to 10% underweight in December. EM had been the most favored region (overweight 43% in February 2013) but this fell to +3% in May, and further to 9% underweight in June and 19% underweight in August, the lowest since the survey began in 2001.

- Commodities (-24%): Managers are less underweight commodities, increasing from 31% underweight in December, the third lowest on record. Low commodity exposure goes in hand with skepticism over EEM. Current weighting is 1.7 standard deviations below its 8 year average.

- Currencies: 57% of managers believe the US dollar is undervalued, the 2nd highest proportion ever.

- Macro: 75% expect a stronger global economy over the next 12 months, the highest reading in 3 years. This compares to just 40% in December 2012, on the eve of the current rally.